Buying your first home is a colossal achievement, a dream realized. As we navigate 2026, the landscape of homeownership continues to evolve, presenting both exciting opportunities and new considerations for aspiring homeowners. This isn't just about signing on the dotted line; it's about embarking on a journey that requires careful planning, smart financial decisions, and a proactive approach to maintaining your new sanctuary. Are you ready to turn that "for sale" sign into your "welcome home" mat?

The prospect of owning your first home can feel overwhelming. Between understanding mortgage options, navigating inspections, and budgeting for unexpected costs, it's easy to feel lost in the maze. But fear not! This comprehensive guide is designed to equip you with the essential first time homeowner tips for 2026, ensuring your transition into homeownership is as smooth and rewarding as possible. We'll cover everything from pre-purchase preparation to post-move-in success, empowering you to make informed decisions and build a solid foundation for your future.

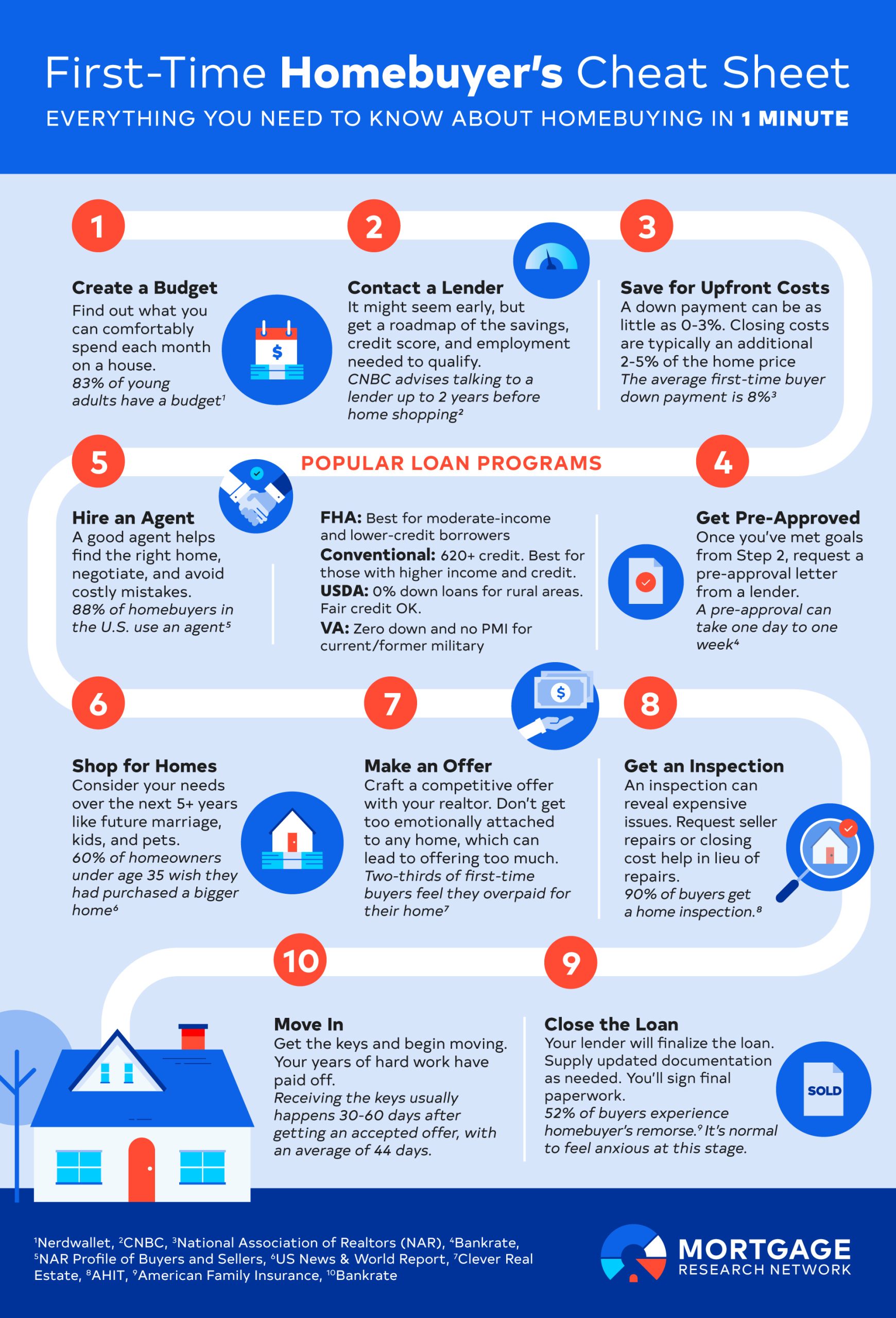

Laying the Financial Foundation: Your Pre-Approval Power-Up

Before you even start browsing listings, the most critical step is to understand your financial standing. This isn't just about knowing how much you want to spend, but how much a lender is willing to lend you, and more importantly, how much you can comfortably afford. In 2026, with fluctuating interest rates and varying market conditions, a strong financial game plan is paramount.

Understanding Your Credit Score: The Gatekeeper of Mortgages

Your credit score is a three-digit number that significantly impacts your ability to secure a mortgage and the interest rate you'll pay. Lenders use it to assess your creditworthiness. A higher score generally translates to better loan terms.

- Aim High: Before applying for a mortgage, strive for a credit score of 740 or higher. This often unlocks the best interest rates.

- Check Your Reports: Obtain your free credit reports annually from each of the three major credit bureaus (Equifax, Experian, and TransUnion) via AnnualCreditReport.com. Review them for any errors and dispute them promptly.

- Responsible Credit Habits: Continue to pay all your bills on time, keep credit utilization low (ideally below 30%), and avoid opening new credit accounts unnecessarily in the months leading up to your mortgage application.

Exploring First-Time Homebuyer Programs and Benefits

The good news is that numerous programs exist to make homeownership more accessible for first-time buyers. In 2026, these resources are more vital than ever.

- Down Payment Assistance (DPA): Many federal, state, and local programs offer grants or forgivable loans to help with your down payment and closing costs. These can significantly reduce the upfront financial burden.

- Government-Backed Loans: Consider FHA (Federal Housing Administration), VA (Department of Veterans Affairs), and USDA (U.S. Department of Agriculture) loans. These often have more flexible credit and down payment requirements, making them ideal for many first-time buyers. For instance, VA loans can offer zero down payment options for eligible veterans.

- Mortgage Credit Certificates (MCCs): Some states offer MCCs, which provide a federal tax credit for a portion of your annual mortgage interest, effectively lowering your tax bill.

- Homeownership Courses: Participating in a HUD-approved homeownership course can not only educate you on the entire buying process but may also qualify you for incentives like lower interest rates or down payment assistance. These courses are invaluable for understanding budgeting, mortgage options, and the responsibilities of homeownership.

Securing Your Mortgage Pre-Approval: The Golden Ticket

Getting mortgage pre-approval is a crucial step. It involves a lender reviewing your financial information to determine how much they are willing to lend you and at what interest rate. This pre-approval letter is essential when making an offer.

- Shop Around: Don't settle for the first lender you speak with. Compare rates and fees from multiple lenders, including banks, credit unions, and online mortgage companies.

- Understand Your Loan Options: Familiarize yourself with different mortgage types, such as fixed-rate mortgages (where the interest rate stays the same for the life of the loan) and adjustable-rate mortgages (ARMs, where the rate can change over time). For 2026, with potential rate fluctuations, understanding the long-term implications of each is key.

- Factor in All Costs: Remember that your monthly mortgage payment includes more than just principal and interest. You'll also have property taxes, homeowners insurance, and potentially Private Mortgage Insurance (PMI) if your down payment is less than 20%.

The House Hunt: Finding Your Perfect Fit

With your finances in order and pre-approval in hand, the exciting part begins: the house hunt! This is where your vision starts to take shape, but it's also a stage where emotions can run high. Staying grounded and focused will help you find a home that meets your needs and budget.

Working with a Real Estate Agent: Your Trusted Advisor

A good real estate agent is an invaluable asset, especially for first-time buyers. They have market knowledge, negotiation skills, and can guide you through the complexities of the transaction.

- Find the Right Fit: Interview several agents to find someone you trust, who understands your needs, and has a proven track record in your desired area.

- Communicate Your Priorities: Be clear about your must-haves, your deal-breakers, and your budget. This will help your agent narrow down the search effectively.

- Listen to Their Expertise: Agents have seen it all. Their insights into neighborhoods, property values, and potential issues can be crucial.

Essential Home Features: Beyond the Curb Appeal

While aesthetics matter, focus on the fundamental aspects of a home that will impact your long-term satisfaction and costs.

- Location, Location, Location: Consider proximity to work, schools, amenities, and transportation. Research the neighborhood's safety, local crime rates, and future development plans.

- The Bones of the House: Pay attention to the roof, foundation, plumbing, and electrical systems. These are expensive to repair or replace, so understanding their condition is vital.

- Layout and Functionality: Does the floor plan suit your lifestyle? Consider the number of bedrooms and bathrooms, the size of the kitchen, and the amount of living space.

- Energy Efficiency: In 2026, energy efficiency is not just environmentally responsible but also a significant cost-saver. Look for homes with good insulation, energy-efficient windows, and modern HVAC systems.

The Crucial Home Inspection: Uncovering Hidden Issues

Never skip the home inspection. This is your opportunity to have a qualified professional assess the property's condition before you commit.

- Choose an Independent Inspector: Select an inspector who is not associated with the seller or your real estate agent.

- Attend the Inspection: Be present during the inspection to ask questions and understand the inspector's findings firsthand.

- Review the Report Carefully: The inspection report will detail any defects, from minor cosmetic issues to major structural problems. Prioritize repairs that affect health, safety, or the structural integrity of the home.

Making the Deal: From Offer to Closing

Once you've found "the one," it's time to make an offer. This stage is a delicate dance of negotiation and paperwork, culminating in the transfer of ownership.

Crafting a Competitive Offer

In a competitive market, a well-crafted offer is essential. Your real estate agent will be instrumental here.

- Offer Price: Based on comparable sales (comps) in the area and the home's condition, your agent will help you determine a competitive offer price.

- Contingencies: Include contingencies in your offer, such as financing, inspection, and appraisal contingencies. These protect you if certain conditions aren't met. For example, an appraisal contingency ensures the home appraises for at least the purchase price.

- Earnest Money Deposit: This is a good-faith deposit that shows you are serious about purchasing the home. It's typically held in escrow and applied towards your down payment or closing costs.

Navigating Closing Costs: The Final Hurdles

Closing costs are fees paid at the time of closing, in addition to your down payment. These can include appraisal fees, title insurance, attorney fees, recording fees, and lender origination fees.

- Budget Accordingly: Closing costs typically range from 2% to 5% of the loan amount. Always factor these into your overall budget.

- Negotiate Where Possible: Some closing costs may be negotiable with the seller, especially if the market is in your favor.

- Review the Closing Disclosure: At least three business days before closing, you'll receive a Closing Disclosure, which outlines all the final costs. Review it meticulously and compare it to your Loan Estimate.

Post-Move-In Essentials: Settling into Homeownership

Congratulations, you're a homeowner! But the journey doesn't end at closing. The first few months and years of homeownership come with new responsibilities and opportunities to make your house truly your own.

Immediate "Must-Dos" for New Homeowners

There are a few critical tasks to tackle right after moving in to ensure your home's safety and security.

- Change the Locks: For your peace of mind and security, change all exterior door locks immediately. This ensures no previous occupants or unknown individuals have keys.

- Locate Your Main Water Shut-Off Valve: Knowing where this is can save your home from significant water damage in case of a plumbing emergency.

- Test Smoke and Carbon Monoxide Detectors: Ensure all detectors are functioning correctly and consider replacing batteries or upgrading to newer models.

- Secure Your Home: Consider upgrading your security system, installing outdoor lighting, or reinforcing entry points.

Establishing a Home Maintenance Routine

Regular home maintenance is key to preserving your investment and avoiding costly repairs down the line. A proactive approach saves money and headaches.

- The 1% Rule: A common guideline is to set aside 1% to 4% of your home's value annually for maintenance and repairs. For a $300,000 home, this means $3,000 to $12,000 per year.

- Create a Maintenance Schedule:

- Monthly: Check and clean HVAC filters, test smoke detectors.

- Quarterly: Inspect and clean gutters, check for leaks under sinks and around toilets.

- Semi-Annually: Inspect the roof and foundation for cracks, service your HVAC system.

- Annually: Clean out the chimney (if applicable), inspect the exterior for pest issues, service your water heater.

- Prioritize Repairs: Address any issues highlighted in your inspection report first. Then, tackle smaller, ongoing maintenance tasks to prevent bigger problems.

Budgeting for the Unexpected: The Homeowner's Emergency Fund

Even with the best planning, unexpected home repairs can arise. Having an emergency fund specifically for home-related issues is crucial.

- Start Small: Aim to build a fund that can cover at least a few months of your mortgage payments and essential living expenses.

- Replenish Regularly: If you use your emergency fund for a repair, make a plan to replenish it as soon as possible.

Making Your House a Home: Personalization and Upgrades

Now for the fun part! As you settle in, you'll want to personalize your space and make upgrades that enhance your comfort and the home's value.

- DIY vs. Professional: For smaller projects like painting or minor repairs, consider DIY. For more complex tasks like electrical work or major renovations, hire a qualified professional.

- Prioritize Smart Upgrades: Focus on upgrades that offer a good return on investment, such as kitchen and bathroom remodels, improving curb appeal, or energy-efficient upgrades.

- Budget for Decor: Don't forget to budget for furniture, decor, and landscaping to truly make your house feel like a home.

First-Time Homeowner FAQs

Q1: How much should I budget for closing costs when buying my first home in 2026?

A1: Closing costs typically range from 2% to 5% of the loan amount. This can include fees for appraisal, title insurance, loan origination, attorney services, and more. It's essential to get a detailed estimate from your lender early in the process and include this in your overall home buying budget.

Q2: What's the biggest mistake first-time homebuyers make?

A2: One of the most common mistakes is not getting pre-approved for a mortgage early on. This can lead to looking at homes outside your budget or falling in love with a property you can't afford. Another significant error is skipping the home inspection, which can lead to costly surprises down the road.

Q3: How much should I save for a down payment in 2026?

A3: While a 20% down payment can help you avoid Private Mortgage Insurance (PMI), many first-time buyer programs allow for much lower down payments, sometimes as low as 3% to 5%. Government-backed loans like FHA and VA loans can have even more flexible requirements. The key is to save as much as you comfortably can, as a larger down payment reduces your loan amount and monthly payments.

Q4: Is it worth it to get a home warranty for my first home?

A4: A home warranty can be a wise investment for first-time homeowners, especially if your home is older or has systems you're unfamiliar with. It can cover the cost of repairs or replacements for major appliances and systems (like HVAC, plumbing, and electrical) that break down due to normal wear and tear. While it's an additional monthly cost, it can provide peace of mind and protect you from unexpected, large repair bills.

Q5: What are the ongoing costs of homeownership beyond the mortgage?

A5: Beyond your mortgage payment, you'll need to budget for property taxes, homeowners insurance, utilities (electricity, gas, water, internet), and regular home maintenance. Don't forget to factor in potential HOA fees if you're buying in a community with a homeowners association, and set aside funds for unexpected repairs.

Conclusion: Your Homeownership Journey Begins Now!

Becoming a first-time homeowner in 2026 is an incredible milestone. By arming yourself with knowledge, staying organized, and approaching the process with a strategic mindset, you can navigate the complexities with confidence. From meticulously planning your finances and understanding mortgage options to diligently inspecting potential homes and establishing a robust maintenance routine, every step contributes to a successful and rewarding homeownership experience.

Remember, this is just the beginning of your journey. Embrace the learning process, celebrate your achievements, and don't hesitate to seek advice from professionals and trusted resources. Your first home is more than just a structure; it's a place where memories will be made, dreams will flourish, and your future will be built. Welcome home!

References

- Redfin — 21 Essential Tips for First-Time Homebuyers, 2025

- NerdWallet — Tips for First-Time Home Buyers

- Bankrate — First-Time Homebuyer Guide

- Budget Dumpster — 11 Must-Know Tips for First-Time Homeowners

- Zillow — New Homeowner Checklist: 20 Things to Do When Moving to a New Home

- Forbes Advisor — 8 Tips For First-Time Homebuyers

- HomeLight — 25 First Time Home Buyer Tips to Get Your Foot in The Door

- Maronda Homes — First Time Homebuyer